by Carlos J. Ochoa (c)

Executive vision: the 5 megatrends shaping videogames 2026–2031

The videogames industry is no longer only a games industry. It is becoming the operating system of digital entertainment: IP, social identity, AI creation, live events, education, esports, creator economies and immersive worlds are converging. Newzoo estimates the global games market at $188.8B in 2025, with 3.6B players, led by mobile but with renewed console momentum after new hardware cycles. PwC expects global videogame revenue to grow from $224B in 2024 to nearly $300B in 2029, exceeding movies and music combined. (Newzoo)

1. From games to transmedia entertainment ecosystems

The winning companies will not sell “a game”; they will build living entertainment universes across games, film, anime, music, live events, merchandise, UGC and communities.

Sony is very clear on this direction: its corporate strategy focuses on a “Creative Entertainment Vision,” maximizing IP value and connecting fan communities across entertainment sectors, with PlayStation as one part of a broader content and creation ecosystem. (Sony) Nintendo follows a different but equally powerful model: protect family-friendly IP, extend it through hardware, software, movies, theme parks and long-tail evergreen franchises. Microsoft’s strategic framing is more platform-led: gaming experiences “on any device,” reinforced by Windows, cloud, Game Pass and Xbox. (Microsoft)

Strategic implication: the future leader is not the studio with the best launch week; it is the company that can sustain an IP universe for 5–10 years.

Key success factors: iconic IP, cross-platform storytelling, community retention, live operations, merchandising, audiovisual partnerships, and the ability to turn players into long-term fans.

2. AI-native game production and personalized play

AI will reshape every layer of the value chain: concept art, coding, QA, localization, NPC behavior, synthetic assets, marketing, personalization, moderation and dynamic content generation.

Tencent explicitly says AI improved ad targeting and supported more engagement with games, while also funding larger AI investments and infrastructure. (static.www.tencent.com) PwC also identifies AI and hyper-personalization as major drivers of advertising and entertainment revenue growth. (PwC)

For AAA studios, AI means faster production pipelines and more efficient live operations. For indie studios, it lowers barriers to entry. For platforms, it means better recommendation, personalization, monetization and safety. For players, it means worlds that adapt to them.

Strategic implication: AI will not simply reduce costs; it will create a new category of adaptive games, where story, difficulty, characters, learning curves and monetization can be personalized in real time.

Key success factors: proprietary data, ethical AI use, creator rights, transparent synthetic content policies, AI-assisted production workflows, and differentiated human creativity.

3. The player becomes creator, co-designer and distributor

The gamer’s role is evolving from consumer to co-creator, performer, modder, streamer, curator, community leader and entrepreneur. UGC is becoming one of the most important strategic battlegrounds. Research on user-generated content in games describes a shift from one-directional entertainment toward collaborative, user-driven ecosystems. (arXiv)

This is already visible in Roblox, Fortnite Creative, Minecraft, Dreams-style creation, modding communities, esports broadcasting, TikTok discovery, Discord communities and creator-led economies. The next step is AI-assisted UGC: players will create levels, characters, missions, music, skins, cinematics and even game modes through natural language.

Strategic implication: the most valuable gamer is not only the one who pays; it is the one who creates value for other players.

Key success factors: easy creator tools, revenue sharing, moderation, IP governance, social discovery, creator analytics, marketplace infrastructure and community trust.

4. Platform convergence: console, PC, mobile, cloud and social video merge

The old borders are disappearing. Console publishers launch on PC. Mobile publishers build console-quality experiences. PC games use live-service mechanics. Cloud allows play across devices. Social platforms become discovery engines. Games become places to watch, chat, shop, learn and attend events.

Newzoo’s 2025 data shows mobile still dominates with $103B, or 55% of the market, while console is the fastest-growing platform in 2025, supported by new hardware cycles and stronger releases. PC remains stable, with momentum in China and Japan. (Newzoo) Deloitte also notes that younger audiences distribute their entertainment time across streaming, social video, gaming, music and UGC rather than one dominant format. (Deloitte)

Strategic implication: the winning strategy is no longer “console versus mobile” or “premium versus free-to-play.” It is right content, right device, right community, right monetization model.

Key success factors: cross-play, cross-progression, scalable engines, flexible pricing, cloud readiness, low-friction onboarding, regional payments and community portability.

5. Regionalization: global IP, local culture, mobile-first growth and new power centers

The next five years will be shaped by regional asymmetry.

North America will remain strong in AAA, platforms, creator economies, streaming and IP consolidation. Microsoft, Take-Two, EA, Epic, Roblox and major entertainment groups will drive convergence between games, social media and Hollywood-style IP.

Japan and Korea will continue to define premium console, character IP, gacha/live-service mechanics, anime-game convergence and high-retention fandom models. Sony and Nintendo remain central, while Korean publishers keep expanding globally through RPGs, MMOs and mobile-first live operations.

China will remain one of the most powerful ecosystems through Tencent and NetEase, with deep expertise in mobile, super-app ecosystems, AI, payments, esports and international investment. Tencent’s 2025 results show how AI, games engagement, advertising and cloud are increasingly interconnected. (static.www.tencent.com)

Europe has a strategic opportunity in AA/indie excellence, cultural IP, serious games, education, simulation, XR, ethical AI and public-sector innovation. Its weakness is scale; its strength is creativity, cultural diversity and regulatory leadership.

MENA, India, Southeast Asia and Latin America will be growth regions for mobile-first gaming, esports, creator communities, youth entertainment and local-language content. PwC notes that developing markets are expected to lead entertainment and media growth rates, with China growing faster than the US in the outlook period. (PwC)

Strategic implication: global success will require regional cultural intelligence, not just translation.

Key success factors: local partners, local creators, mobile optimization, flexible monetization, cultural adaptation, esports communities, payment localization and government relations.

The new role of gamers

The gamer of the next decade is not passive. The gamer becomes:

1. Co-creator — building maps, skins, missions, mods, stories and AI-generated content.

2. Community amplifier — driving discovery through TikTok, Twitch, YouTube, Discord, Reddit and in-game social graphs.

3. Economic actor — buying, selling, subscribing, donating, tipping, collecting, promoting and sometimes earning inside gaming ecosystems.

4. Data partner — shaping personalization, recommendations, difficulty, matchmaking and monetization through behavior.

5. Cultural protagonist — transforming games into identity, lifestyle, fandom, education, social belonging and creative expression.

The most important strategic shift is this: the gamer is no longer the end of the value chain; the gamer is part of the production, marketing, distribution and innovation system.

Final strategic conclusion

The next five years will reward companies that understand videogames as living cultural ecosystems, not isolated products. The winners will combine:

strong IP + AI-native production + creator economies + cross-platform access + regional cultural intelligence.

The new competitive advantage will not only be technology. It will be the ability to create belonging, participation and emotional ownership among players. In this new scenario, gamers are not just audiences. They are creators, ambassadors, communities, competitors, investors of attention and co-authors of the future of entertainment.

Strategic role for the Spanish videogame industry

Spain should not try to compete head-to-head with the United States, China, Japan or Korea in pure scale. Its opportunity is different: Spain can become a specialized European hub for culturally distinctive, socially meaningful, transmedia and creator-driven videogame experiences.

Spain already has strong foundations: the Spanish consumer market reached around €2.4B in 2024, with 22M players, and women slightly outnumbering men among players for the first time in AEVI’s 2024 data. On the development side, the 2025 DEV White Paper reports €1.464B in turnover in 2024, more than 10,500 jobs, and 52% of revenue coming from international markets. But the ecosystem remains fragile: many studios are small, financing is limited, and DEV reports that funding is the main challenge for around 80% of studios. (Cine y Tele)

Spain’s strategic position: a bridge, not a periphery

Spain can play five key roles in the global industry:

1. The European–LATAM bridge

Spain has a natural cultural and linguistic advantage with Latin America. This is one of its strongest strategic assets.

Spanish studios, publishers, accelerators and institutions should position Spain as the gateway between European production standards and Spanish-speaking global audiences. This includes localization, community management, esports, creator campaigns, educational games, mobile-first formats and culturally relevant IP.

Strategic opportunity: build games and platforms for a Spanish-speaking market of hundreds of millions, not only for the domestic market.

2. The cultural IP and transmedia laboratory

Spain has extraordinary cultural assets: history, architecture, literature, music, sport, gastronomy, mythology, festivals, heritage, cities and creative industries. These can become videogame IP, immersive experiences, animation, series, digital collectibles, live events and educational content.

Spain should not only produce “games made in Spain.” It should produce Spanish-origin worlds with global emotional appeal…or better Games Made in EU !!!

Potential areas include historical adventure, fantasy inspired by Iberian and Mediterranean culture, music-based games, art games, educational worlds, tourism gamification, cultural heritage XR, and family-friendly transmedia IP.

Strategic opportunity: become Europe’s leading hub for cultural videogame IP, connecting videogames with film, museums, tourism, music, education and public institutions.

3. The indie, AA and premium creative hub

Spain has already shown strong creative capacity through internationally recognized titles and studios. Its most realistic competitive field is not massive AAA domination, but high-quality indie, AA and premium niche games.

This aligns with global market shifts: PC and digital storefronts increasingly allow smaller, distinctive titles to reach international audiences. Recent Newzoo analysis notes that lower-priced PC releases are reshaping spending patterns, particularly benefiting indie and emerging developers. (GamesRadar+)

Spain should double down on: quality art direction, emotional storytelling, distinctive mechanics, serious games, simulation, strategy, horror, narrative adventure, music and educational experiences.

Strategic opportunity: position Spain as a “boutique powerhouse” for creative, original, exportable games.

4. The serious games, education and XR innovation hub

Spain has a major opportunity in the intersection of videogames, education, training, XR, health, culture and public services.

This is not secondary. It is strategic. As AI, immersive technologies and gamified learning evolve, the boundary between videogames, simulation and education will continue to blur. Spain can lead in game-based learning, immersive classrooms, cultural heritage experiences, digital twins, vocational training, language learning, healthcare training and senior wellbeing.

This is especially relevant because Europe has strong public education systems, cultural institutions and public innovation programs. Spain can use public-private collaboration to turn serious games and XR into an exportable specialization.

Strategic opportunity: make Spain a European reference in games for learning, culture, wellbeing and social impact.

5. The human-centered AI and creator-economy testbed

AI will lower production costs and expand creative possibilities. For Spain, this is a major opportunity because many studios are small and underfinanced. AI can help them produce faster, localize better, prototype earlier, test more efficiently and compete internationally.

But Spain should avoid becoming a low-cost AI-content factory. Its advantage should be human creativity amplified by AI, not generic AI production.

The most promising model is: small creative teams + AI-assisted workflows + community co-creation + strong art direction + global digital distribution.

Strategic opportunity: become a European reference for ethical, human-centered AI in game creation and creator tools.

Spain’s role by sector

- AAA: Talent provider, co-development partner, outsourcing specialist, localization hub, selective original IP

- AA / Indie: Main creative battlefield: distinctive, artistic, narrative, cultural and premium games

- Mobile: Strong opportunity in Spanish-speaking markets, casual games, educational games and community-driven formats

- Esports: Regional bridge between Europe and LATAM; events, communities, clubs, education and branded entertainment

- XR / Immersive: Culture, music, museums, education, training, tourism and location-based entertainment

- Serious games: One of Spain’s strongest future positions: education, health, public sector, skills and simulation

- AI tools: Small-studio acceleration, localization, QA, procedural production and creator platforms

Spain’s role by region

In Europe, Spain should position itself as a creative and cultural production hub, especially for indie, AA, XR, education and public-sector innovation.

With Latin America, Spain should become the commercial, linguistic and cultural bridge: publishing, distribution, esports, creator networks, localization and co-production.

With North America, Spain should act as a creative partner for IP development, art direction, co-development, European market access and culturally distinctive experiences.

With Asia, Spain should look for partnerships in mobile, anime/game convergence, character IP, monetization models, hardware, esports and transmedia development.

With MENA, Spain has an opportunity in education, youth entertainment, esports, tourism, smart cities, cultural heritage and immersive experiences.

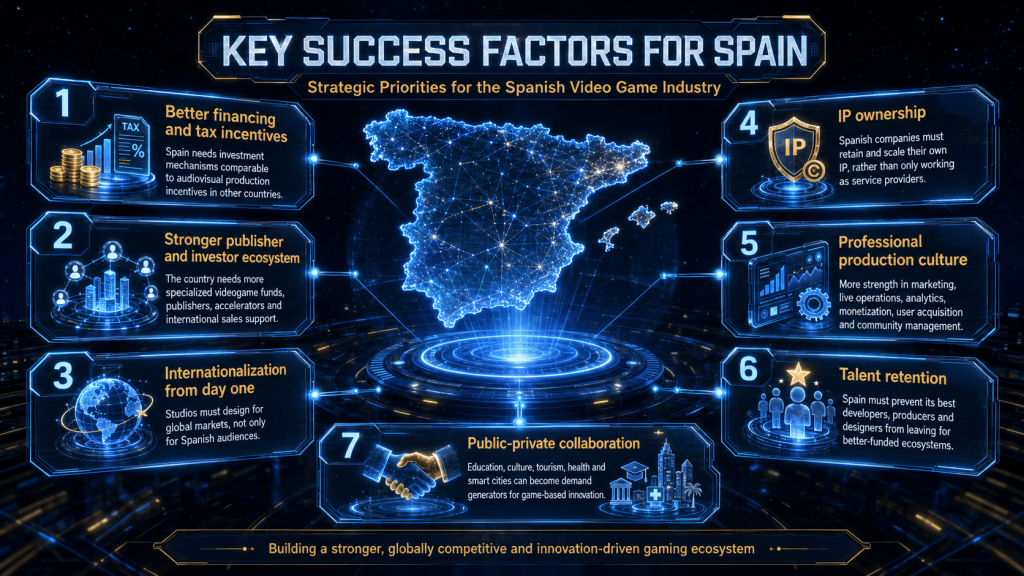

Key success factors for Spain

Spain needs to solve one structural issue: talent exists, but scale and financing are insufficient. The sector has creativity and international potential, but many studios remain small and fragile. Reports around the 2025 DEV White Paper highlight the concentration of activity in Catalonia and Madrid, the dominance of small studios, the importance of exports, and the continuing need for financing and public incentives. (Cadena SER)

The key success factors are:

1. Better financing and tax incentives Spain needs investment mechanisms comparable to audiovisual production incentives in other countries.

2. Stronger publisher and investor ecosystem The country needs more specialized videogame funds, publishers, accelerators and international sales support.

3. Internationalization from day one Studios must design for global markets, not only for Spanish audiences.

4. IP ownership Spanish companies must retain and scale their own IP, rather than only working as service providers.

5. Professional production culture More strength in marketing, live operations, analytics, monetization, user acquisition and community management.

6. Talent retention Spain must prevent its best developers, producers and designers from leaving for better-funded ecosystems.

7. Public-private collaboration Education, culture, tourism, health and smart cities can become demand generators for game-based innovation.

The new role of Spanish gamers

Spanish gamers are not only consumers. They are becoming:

- community builders, through Twitch, YouTube, Discord, TikTok and esports;

- cultural ambassadors, because Spanish-language creators can reach Spain and Latin America;

- co-creators, through mods, UGC, Roblox/Fortnite-style platforms and AI-assisted creation;

- test communities, helping studios validate mechanics, narratives and monetization;

- educational users, because videogames are entering classrooms, museums, training and cultural experiences;

- and market shapers, because Spain’s player base is large, diverse and increasingly gender-balanced. (Cine y Tele)

The Spanish gamer can become one of the industry’s greatest strategic assets: a bridge between European creativity and the global Spanish-speaking digital culture.

Final strategic thesis

The role of the Spanish videogame industry should be:

to become the European creative bridge to the Spanish-speaking world, leading in cultural IP, indie/AA excellence, serious games, XR, education, transmedia storytelling and human-centered AI.

Spain will not win by being the biggest. Spain can win by being the most culturally distinctive, emotionally intelligent, internationally connected and socially meaningful videogame ecosystem in Europe.

Reference Sources

- Newzoo — Global Games Market Report 2025 Global market, platforms, number of players, mobile/console/PC evolution, and forecasts.

- PwC — Global Entertainment & Media Outlook 2025–2029 Global growth in entertainment, video games, media, advertising, AI, and emerging markets.

- Deloitte — Digital Media Trends 2025 Digital consumption habits, younger audiences, gaming, streaming, social video, and the attention economy.

- Sony Group — Corporate Strategy / Creative Entertainment Vision 2025 IP strategy, transmedia entertainment, PlayStation, music, film, anime, and communities.

- Microsoft — Annual Report 2025 / Xbox & Gaming Strategy Game Pass, cloud gaming, Activision Blizzard, content, services, AI, and multiplatform infrastructure.

- Tencent — Annual Results / Corporate Reporting 2025 Mobile gaming, AI, advertising, social entertainment, cloud, China, and digital ecosystems.

- Nintendo — Corporate Reports / IP Strategy Intellectual property, hardware, software, family-friendly franchises, films, theme parks, and transmedia expansion.

- DEV — White Paper on Spanish Video Game Development 2025 Spanish game development: revenue, employment, internationalization, funding, and structural challenges.

- AEVI — The Video Game Industry in Spain. Yearbook 2024 Spanish consumer market, number of players, revenue, gamer profile, and sector evolution.

- Spain Audiovisual Hub / ICEX / Red.es Public programs, internationalization, funding, audiovisual sector, video games, and Spain’s positioning.

- EGDF — European Games Developer Federation European comparison, public policies, incentives, regulation, and competitiveness of European game development.

- GamesIndustry.biz / GDC State of the Game Industry Development trends, investment, publishing, layoffs, AI, game engines, funding, and studio perceptions.

- Sensor Tower / data.ai Mobile gaming, monetization, user acquisition, retention, regional markets, and user behavior.

- Steam / Steamworks Reports PC gaming, digital distribution, indie games, early access, wishlist economy, and purchasing behavior.

- Roblox, Epic Games / Unreal Editor for Fortnite, Minecraft Education UGC, creator economy, social experiences, education, communities, and the new role of the player-creator.

Carlos J. Ochoa (c)